Why Agency MBS May Be the Hedge Investors Need in an Uncertain Market Environment

Will the Fed raise rates or let the market cycle play out? Is inflation resurgent or are we really just seeing “base effects” that reflect distorted year-over-year comparisons to the COVID era? Will the Fed taper or continue to support the Agency Mortgage Backed Securities (“MBS”) and Treasury markets with tens of billions of dollars of monthly purchases? And will the historically high prices and tight spreads across markets persist?

It likely may be weeks or even months before we have clear signals as to these major directional moves, in which case perhaps the most important question is: what can investors do now to ensure they are well positioned in an increasingly uncertain environment?

While in our view a majority of paths seem biased toward higher rates, we think there are alternative scenarios where the rise in inflation is transitory and rates ending up falling from here. But what if higher inflation does, in fact, take hold and the Fed determines its current policies are no longer appropriate?

Investors across the globe remain heavily exposed to fixed income instruments and strategies that benefit from the prevailing conditions of very low rates, depressed volatility, and the continuance of historically tight spreads. We believe that elevated valuations of all types of assets are inextricably tied to the Federal Reserve maintaining its zero-interest rate policy and large scale MBS and Treasury purchases.

At current valuations, we think Agency MBS pass-throughs are at serious risk of a major re-pricing in the coming months/years, whether it’s from Fed tapering, higher rates, rising inflation, increased volatility, or private investors simply requiring more compensation to own MBS (or perhaps some combination of all these).

Prudent investors should be seeking ways to protect themselves from the possibility of a correction in risk markets. In our view, the Agency MBS market currently provides liquid and relatively inexpensive ways through the multi-trillion dollar TBA market to construct trades that benefit from shifting market dynamics, especially increased volatility and the Federal Reserve tapering it’s $40 billion+ of monthly MBS purchases.

Shorting the Agency MBS Basis (“Short MBS Basis”)

Short MBS Basis May Be the Lifeline Investors Need

Specifically, we are referencing what us Agency folks call the Short Basis. In its most basic form, the Short Basis is implemented by shorting the current coupon TBA pass-through while going long a similar duration Treasury (e.g., short Fannie Mae 2.0% TBA vs long 7-Year U.S. Treasury). This is a neutral duration, long volatility trade that benefits if the spread between the Agency MBS and the Treasury widens (i.e., increases).

Chapter 1, paragraph 1 in any mortgage primer tells you that investors demand incremental yield to own MBS versus a U.S. Treasury. MBS have drifting durations and inherent negative convexity (more downside than upside) due to the prepayment option of borrowers. MBS entail more risk so the prevailing wisdom is that an investor should get “paid” to own mortgages in lieu of a positively convex, government-guaranteed U.S. Treasury.

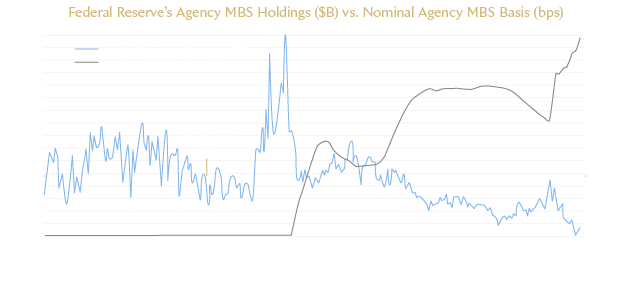

Fast forward to today and the spread between Agency MBS and Treasuries is almost non-existent (see below), which means the cost to maintain this Short Basis position is quite low. The abnormally tight spread level is largely the result of the Federal Reserve’s most recent round of pandemic-related QE, where they lapped up nearly $1 TRILLION of MBS since March 2020.

While predicting the exact timing of spread normalization is impossible, we are highly convicted that the current level of Agency MBS spreads is unsustainable over the long-term. Regardless of the spread metric one chooses, Agency MBS are sitting at the most egregiously tight levels in the 30+ year history of the mortgage market. As an example, the current coupon Fannie Mae MBS is offering a mere 60 bps more than 7-year Treasuries, which is evidenced in the graph below.

Option-Adjusted Spreads (“OAS”) are even more eye-popping. A few steps further than the nominal spread, OAS takes into account the cost of hedging a negatively convex MBS (i.e., the hedge-adjusted spread). Currently, that same Fannie Mae current coupon is trading at -16 bps OAS. In theory, if you “perfectly” hedged this bond, you would be guaranteed to lose money over a 1-year horizon.

Further tightening is certainly possible if an investor wants to make the gamble that the Fed is in the midst of permanent MBS QE, but as a wise mortgage market sage once said, “Hope is a personal virtue, but a terrible investment strategy.” There’s little to no meat left on the bone, so with or without the Federal Reserve devouring all the supply, we aren’t sure who the marginal buyer is likely to be until there is substantial cheapening of these assets.

Fed Tapering

Painful For Agency MBS

Since the Federal Reserve re-initiated Agency MBS purchases in response to the COVID-19 pandemic last March, it has absorbed all of the total net issuance of Agency MBS (and then some!). The formidable combination of demand from both the Fed and U.S. banks (who needed a capital efficient place to park their swelling base of deposits from stimulus checks) drove valuations to the historical levels discussed above.

To put the Fed’s enormous buying spree into perspective, they are currently buying every single newly issued MBS as well as also buying mortgages that are flooding the market from other participants who continue to sell.

While Fed messaging has only recently started to suggest the possibility of tapering MBS purchases, we believe it’s a realistic scenario and possibly one that could unfold in the second half of 2021 and beyond. It’s hard to imagine where less Fed buying does not have a severe impact on mortgage spreads from today’s levels.

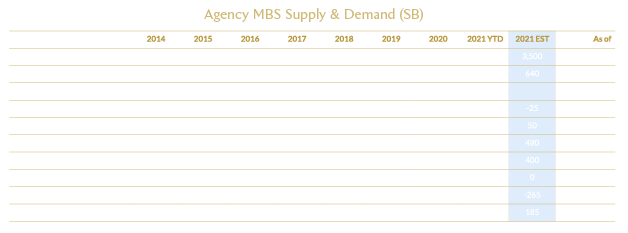

In the figure below from Morgan Stanley Research, estimated net supply for 2021 is $640B (supply has been trending higher of late given very low mortgage rates and a white-hot housing market). If you exclude the Federal Reserve bid for MBS from the other sources of demand (Overseas, Banks, REITs, and Money Managers) there’s a gaping $480B hole that would need to be absorbed by private investors. Who is that likely to be when 10-year Treasuries have yields of 1.5% that are on top of Agency MBS at 1.8%? Money Managers have been large net sellers in the current environment and likely need more spread to justify a meaningful growth in allocation to this asset class.

The Holy Grail

A Cheap Hedge That Can Ride the Waves of Volatility

We believe the timing is now: Agency MBS are historically rich to Treasuries, and the cost of shorting them is low. For investors with diverse portfolios that are exposed to the macro-economic currents outlined in this piece, there are few good options to get long volatility and benefit directly from Fed tapering.

As investors seek shelter from a possible gathering storm of rising rates, rising inflation, a tapering of QE, and tight spreads, our view is that the Short Basis position provides investors with asymmetric risk-reward and the means to alleviate the portfolio destruction that could occur if some or all of the aforementioned risks play out.