An overlooked asset class may be the cure for investors with a case of private credit indigestion

OVERVIEW / For allocators to private credit concerned about transparency and liquidity issues, seasoned CMBS may represent an attractive opportunity to use those attributes with current pricing, making a compelling entry point.

AUTHORS / Bob Neighoff and Evan Kurtz, Portfolio Managers, Cicero, a Mariner PM Team. Cicero is an investment team within Mariner focused on CMBS.

An Appetizing Sub-Sector of Fixed Income

In light of the questions currently being asked of private credit, one subsector frequently overlooked by those seeking the potential for superior returns to high yield corporate debt, but with increased liquidity and price discovery, is the ~$700 billion seasoned private label CMBS market.

Seasoned CMBS are securities at the tail end of their term (Cicero focuses on those with ~2-3 years until maturity). This means they have an established history of payment and property-level metrics that de-risk the investment and, for those such as Cicero with the requisite expertise and resources, enable deeper diligence and analysis.

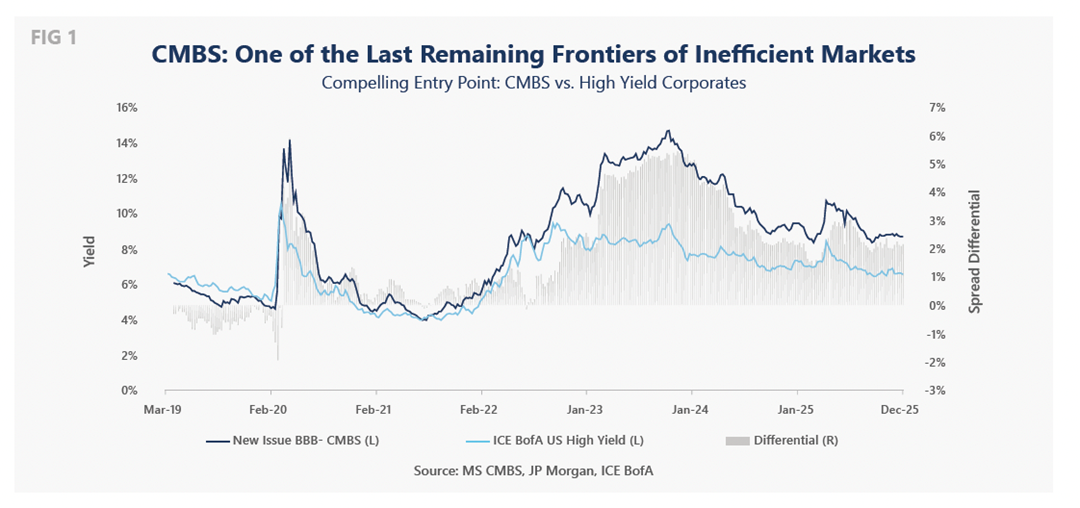

We have spent decades in the space and view it as one of the last remaining frontiers of inefficient markets, which also currently offers a compelling entry point with wider spreads to HY Corporates (See Fig. 1). In our view, investors can access these attractive spreads and total return potential from pull to par on bonds trading at a discount. These offer much greater downside protection through thorough underwriting and management of known, analyzable risks than in private credit. In the latter, the threats to terminal value from AI, among other headwinds, are still far from being understood.

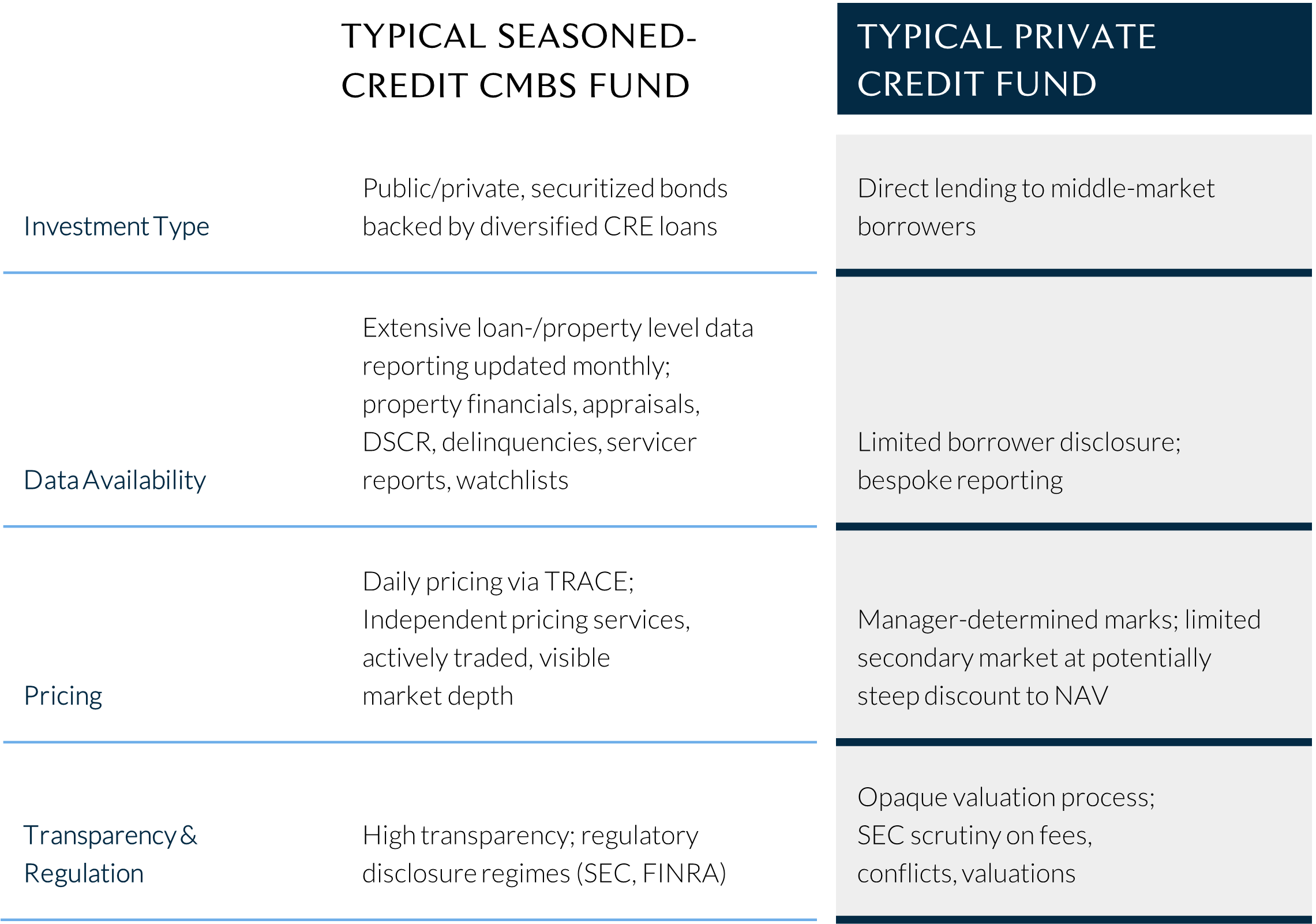

Importantly, at a time when investors may be concerned by wide dispersions between the valuations of their private credit investments and the trading levels of public market comparables, CMBS provides daily price discovery and liquidity that can be observed via TRACE and various independent pricing services broadly relied upon across institutional market participants. This vibrant market for CMBS also creates the opportunity to enhance the asset class’s already attractive yields through active trading. This has been a substantial contributor to our success over many years as we navigated major market dislocations, including the dotcom and telecom bubbles, the Global Financial Crisis (“GFC”), the 2010s sectoral recessions in energy and retail, COVID and the work-from-home shift, and the recent interest rate hiking cycle.

CMBS vs. Private Credit: Different flavors

The private credit market has grown beyond $2 trillion with no end in sight; over the past decade it has evolved to become an important part of the overall credit landscape. However, as it expands, regulators and allocators are increasingly focused on important questions relating to valuation transparency, data availability, and potential system linkages as bank financing to private credit vehicles continues to rise.

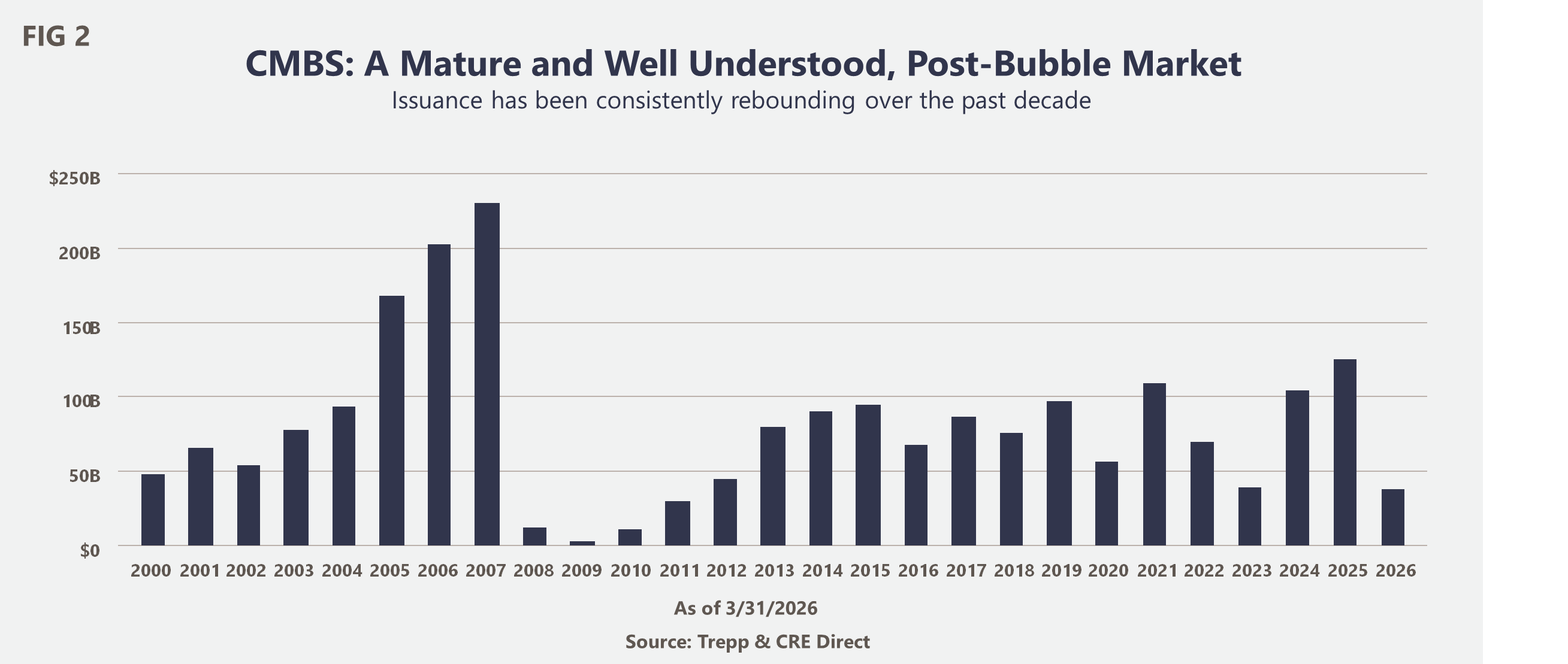

Against this backdrop, consider that the CMBS market today sits at approximately $699 billion, well below its peak of over $900 billion immediately prior to the GFC. Issuance has been consistently rebounding over the past decade (albeit with an understandable interruption to this trend due to COVID), underscoring continued liquidity and investor confidence in public securitized credit markets (See Fig. 2). Today, this is a mature and well understood, post-bubble market.

Transparency, liquidity, and real-time price discovery form a three-fold advantage vs. less liquid alternative strategies. From an information disclosure perspective, CMBS investors benefit from monthly remits, loan-level reporting, and TRACE-observable trading, enabling price-based risk management. Seasoned CMBS bonds offer additional data and context through paydown history and observable collateral performance, further supported by third-party surveillance from rating agencies.

We do not view private credit as providing a sufficient premium for the illiquidity currently, and allocators still on the fence about seasoned CMBS might consider that the latter also offers more diversification from broad equity and high yield corporate credit markets than direct lending achieves, which can benefit portfolio construction.

In fairness, CMBS experiences credit cycles like any asset class, but the delinquencies caused by COVID-led shifts in where people worked and lived, together with the rate shock of 2022, were clearly visible and instantly reflected in market pricing. Despite some near-term spread widening in CMBS from the Iran war shock, we don’t see this fundamentally impacting the CRE space and in fact we believe it presented an opportunity to invest in some high-quality assets at what we viewed as dislocated discounts. We believe the recovery that began in 2024, and which has seen delinquencies decline from a peak of 10.3% in 2020, is likely to continue.

Another distinction between the recent, and still ongoing, credit cycle in CRE debt and the emergent one in private credit are their respective drivers and how well allocators can reasonably expect their managers to grasp them.

In the past several years, the CMBS market has confronted a global pandemic that turned how people work and live on its head, followed by one of the most rapid rate-hiking cycles ever. This swiftly converted yesterday’s comfortably-levered cashflow machine into tomorrow’s underwater disaster. However, the ultimate drivers behind these swings in CMBS valuations were the same ones that experienced real estate and structured credit investors evaluate every day: where people are renting property, how much they’re willing to pay for it, and how much it costs a building owner to finance their asset. We are confident that we have the information, analytical capabilities, and resources here at Cicero and across the Mariner platform to navigate those factors. Across multiple credit cycles, Cicero’s seasoned CMBS approach has demonstrated resilience through periods of significant market stress.

However, in private credit today the biggest risks—specifically, how the emergent, rapidly evolving technological revolution in AI will impact legacy software companies—are much harder to evaluate and predict.

There is no playbook for this. AI is something that many of the smartest minds, with the largest pools of capital ever assembled by mankind, are shaping, reshaping, and trying to understand every second of every day. Personally, if we endeavored to fully grasp that technological revolution with conviction, confronted the attendant unknowns, and felt that we had done so suitably, we would want to earn “equity-like” returns, as opposed to just interest and principal at maturity.

You Have to Know Your Way Around the Kitchen

Despite our confidence that the primary risks in the CMBS market are well within our capability to manage, it is certainly a space that presents many complexities and inefficiencies. Allocators’ experience will largely be driven by the ability of the manager with whom they partner to capitalize on those inefficiencies. There are few dedicated participants in this area, and it requires real focus for success.

Manager expertise may also help to overcome another curious facet of this niche—namely that CMBS products are subject to inconsistent coverage by the major credit rating agencies. Given some conventional asset managers can be ratings-sensitive, they may become forced sellers when ratings change. This creates potential for specialized managers who are not reliant on ratings and who are capable of forming a fundamental view to better exploit any price dislocations.

Cicero, a specialized investment team within Mariner, falls squarely into this bracket, having spent decades analyzing and investing in these markets, with a particular emphasis on seasoned CMBS bonds. Our work has been underpinned by Cicero’s extensive network of relationships in CRE capital markets, which has allowed us to develop the deep sectoral insights that inform our approach. This is in keeping with the philosophy of the broader Mariner philosophy, which has led to the firm’s evolution into a premier multi-strategy platform focused on uncorrelated, liquidity-conscious returns.

Conclusion: Serving Up Something Special

The seasoned CMBS market stands out for allocators seeking to mitigate some of the challenges of the private direct lending market by increased exposure to an asset class that offers greater transparency, daily liquidity, and real-time price discovery. Over and above these factors, current pricing makes entry an attractive proposition—CMBS spreads are trading at levels we have only seen a handful of times over the 40-year history of the asset class.

Private-label CMBS spreads remain wide relative to long-term averages. At the same time, spreads have already tightened meaningfully from the dislocations observed in 2023–2024, particularly in senior tranches. This creates a favorable entry point, with investors able to capture the benefit from potential price appreciation as spreads continue to normalize.

In part, the CMBS market today reflects more disciplined underwriting standards, including lower leverage and stronger debt service coverage compared to prior cycles. While some pockets of stress remain, the big picture suggests overall credit performance has been more resilient than initially feared, contributing to this ongoing, gradual repricing of risk.

On a medium-term view, we see the macro backdrop also becoming more supportive. Expectations are for greater interest rate stability, and ultimately, policy easing should help reduce volatility and improve investor confidence in fixed-rate credit products.

In short, there are many reasons why allocators would do well to consider this much-overlooked asset class.

Three essential questions allocators must ask

1. Is the upcoming real estate maturity wall a risk?

It is true that a large volume of loans originated in a lower-rate environment will need to be refinanced at materially higher interest rates and, in many cases, at lower property valuations.

However, we regard this as being structurally positive for the CMBS market as a whole. Longer term stronger assets are more likely to refinance successfully, while weaker assets may underperform, but during periods of dislocation, liquidity-driven repricing can push even well-covered bonds wider. This will lead to greater dispersion across both deals and tranches as well, giving the opportunity for selective active managers who can move quickly to buy mispriced bonds with resilient collateral while avoiding deteriorating credits. This dynamic makes it even more important for allocators to partner with proven specialists.

2. Isn’t comparing seasoned CMBS to the current challenges facing private credit comparing apples and oranges? How does CMBS compare to other structured products?

Given widespread market concerns related to the current approach taken by private credit managers, we think it is valid to highlight areas of the market that may have been overlooked and that do not traffic in these same issues. As a general rule, allocators should evaluate the full range of options open to them for providing consistent, high current income and total return potential. We believe seasoned CMBS is one such option.

3. But aren’t private credit coupons usually higher?

Spreads can fluctuate with the market, but it is important to remember that private credit should reward investors with an illiquidity premium over a more liquid instrument, such as a CMBS, as well as for the underlying risk of the asset. We believe seasoned CMBS typically delivers a compelling return profile in terms of the coupon and total return in most market conditions and especially today.

Comparison / Typical Seasoned-Credit CMBS Fund vs Typical Private Credit Fund